Linked by one chain: How blockchain secures data

How does blockchain technology work, which is not only behind cryptocurrencies but also behind real estate transactions, logistics processes, and healthcare?

What is blockchain technology

Blockchain is a technology that allows for the storage and transmission of data in the form of a sequence of linked blocks. Each block contains information and a reference to the previous one, forming a chain. This structure ensures that data in the blockchain is protected from alterations and falsification.

In the blockchain network, there are numerous participants who collaborate to process and confirm transactions. Each node actively participates in verifying and adding new blocks with these transactions.

Let's imagine a family recipe for apple pie that is passed down from generation to generation. Every time new family members learn the recipe, a copy is created and added to the previous copies, forming a chain. If someone decides to modify the recipe, everyone preparing it can see the changes and compare them to the original. As a result, the original recipe remains unchanged.

In real life, blockchain is used for creating alternative currencies like Bitcoin, in finance, medicine, and real estate. Blockchain is structured in a way that allows data to be stored and transmitted without the need for intermediaries.

How Blockchain Works

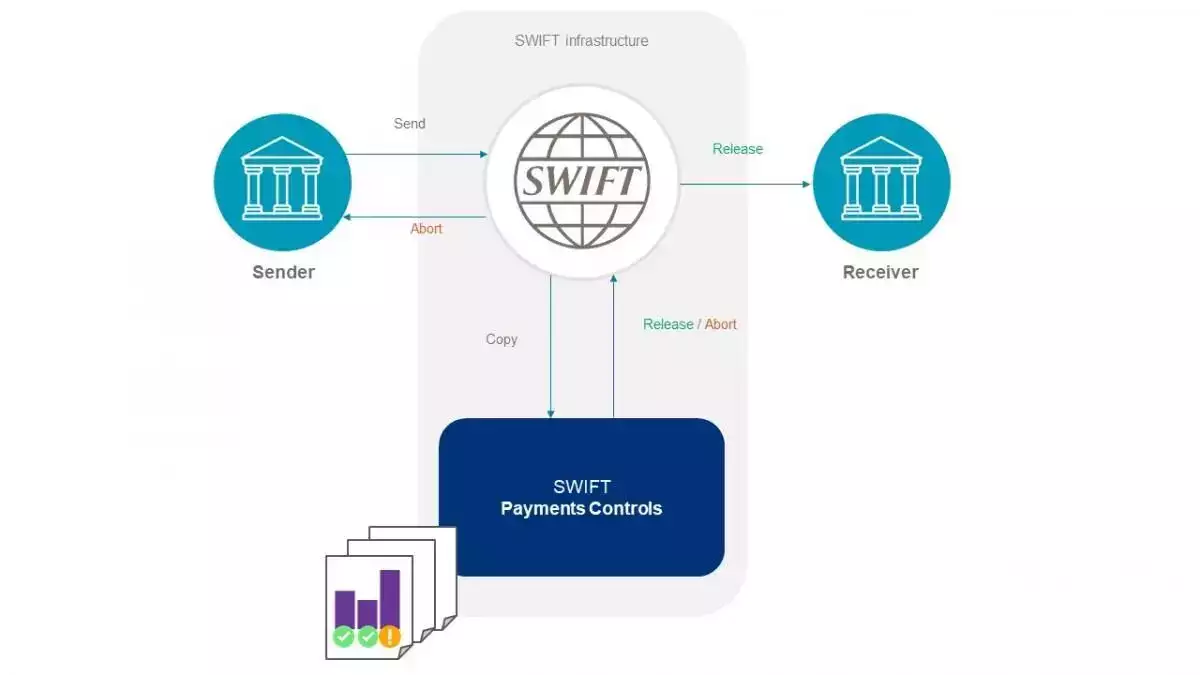

Let's consider how international money transfers operate, both with and without blockchain. Suppose we need to send money to another country. Typically, we would turn to a bank to act as an intermediary in this transfer:

- We provide the bank with information about the recipient and the transfer amount.

- The bank verifies the sender's information.

- If the information is accurate, the bank informs the payment system that the funds can be transferred to the other account.

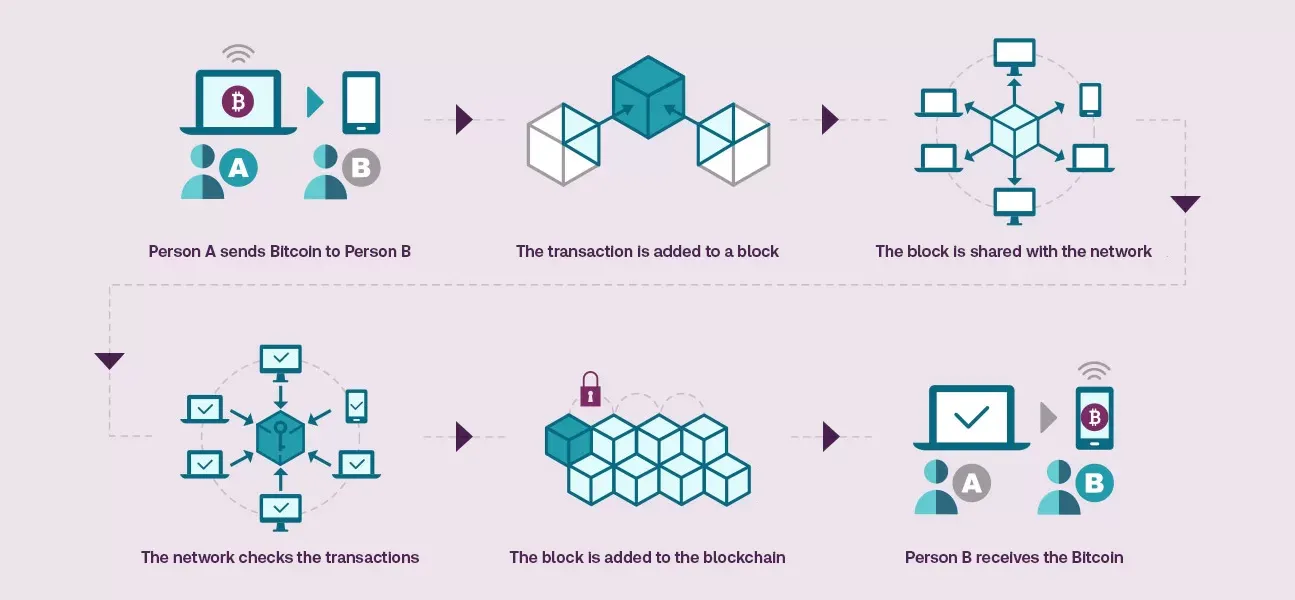

Now, let's imagine transferring money to another country using blockchain. In this case, a bank is unnecessary—security in the transfer is ensured by the blockchain network. Here's how it happens:

Digital Wallet

The internet is an insecure space; revealing banking details for money transfers is risky. A wallet serves as an alternative to a bank account. It can be in the form of an application or a specialized physical device like a flash drive. Instead of traditional currency, these wallets use cryptocurrencies. Digital wallets simplify the sending and receiving of payments. The owner remains anonymous to everyone in the network. When a user creates a wallet, they receive unique addresses for sending and receiving cryptocurrencies. To send money, one needs to specify the recipient's wallet address, the transfer amount, and the fee for including the transaction in the blockchain.

Transaction Signature - An Alternative to PIN Code

After sending transfer data, it's necessary to sign the transaction using a private key. This is a unique secret phrase linking the wallet and the user's assets. The signature guarantees that only the person who owns the private key or knows it can initiate the transaction.

Smart Contracts Instead of Payment Gateways

Payment gateways, the services through which traditional payments pass (e.g., from a buyer to an online store), are replaced by smart contracts in the blockchain. These are various pieces of code containing logic and rules for the automatic execution of payments and transactions. All computers in the blockchain maintain a copy of the smart contract. When a user sends money, the smart contract checks if there are sufficient funds in the account, and in case of errors, it simply cancels the transaction.

Protection Against Malicious Actors through Data Hashing

The encryption algorithm uses information about our transfer and transforms it into a set of characters—this is the hash. The main principle is that any change in the original data leads to a change in the calculated value of the hash.

The original data cannot be easily restored from the hash; encryption key or significant computing power and time for decryption are required. Therefore, the only thing visible in the transaction is the recipient's wallet address.

But blockchain wouldn't be blockchain (from English "blockchain"—a chain of blocks) if it didn't link all previous hashes. This behavior increases the reliability of the entire system and complicates life for malicious actors. In the blockchain, each encrypted record is complemented along with the hash from the previous ones. Thus, all subsequent records depend on those that have already been added to the system. If you change even one, you will have to recalculate the hashes of all previous transactions in the blockchain network, and for that, resources are needed.

Proof of Work (PoW)

resembles a contest to solve a complex mathematical problem. Participants compete to be the first to find the correct solution. Each computer in the network sequentially tries different nonce numbers (a number that can only be used once)—an integer value at which the block's hash will satisfy certain criteria. For example, starting with a certain number of zeros. There can be 100 or 1000 such hash operations, all to find the correct "nonce." When the problem is solved, the block is added to the previous chain, and the transaction becomes immutable.

Proof of Stake (PoS)

is analogous to asset ownership. In PoS, there's no need to solve complex problems as in PoW. Large computational power isn't required, making it easier and cheaper to scale than PoW. Validating participants (analogous to miners in PoW) or stakers are randomly selected based on the amount of cryptocurrency they own. More cryptocurrency means a greater chance of creating a new block. However, PoS contradicts the idea of decentralization, as participants with more cryptocurrency gain more influence in the network.

To develop blockchain projects, one needs to understand the fundamental concepts of blockchain and how smart contracts work, be familiar with languages such as Solidity, Python, Java, or C++ for backend development, and JavaScript for frontend applications. Other skills and requirements may vary depending on the specific blockchain platform and project. Learning a programming language can be done independently, but progress may be faster through specialized courses. Students typically learn in groups with experienced mentors and work on examples from real business scenarios.

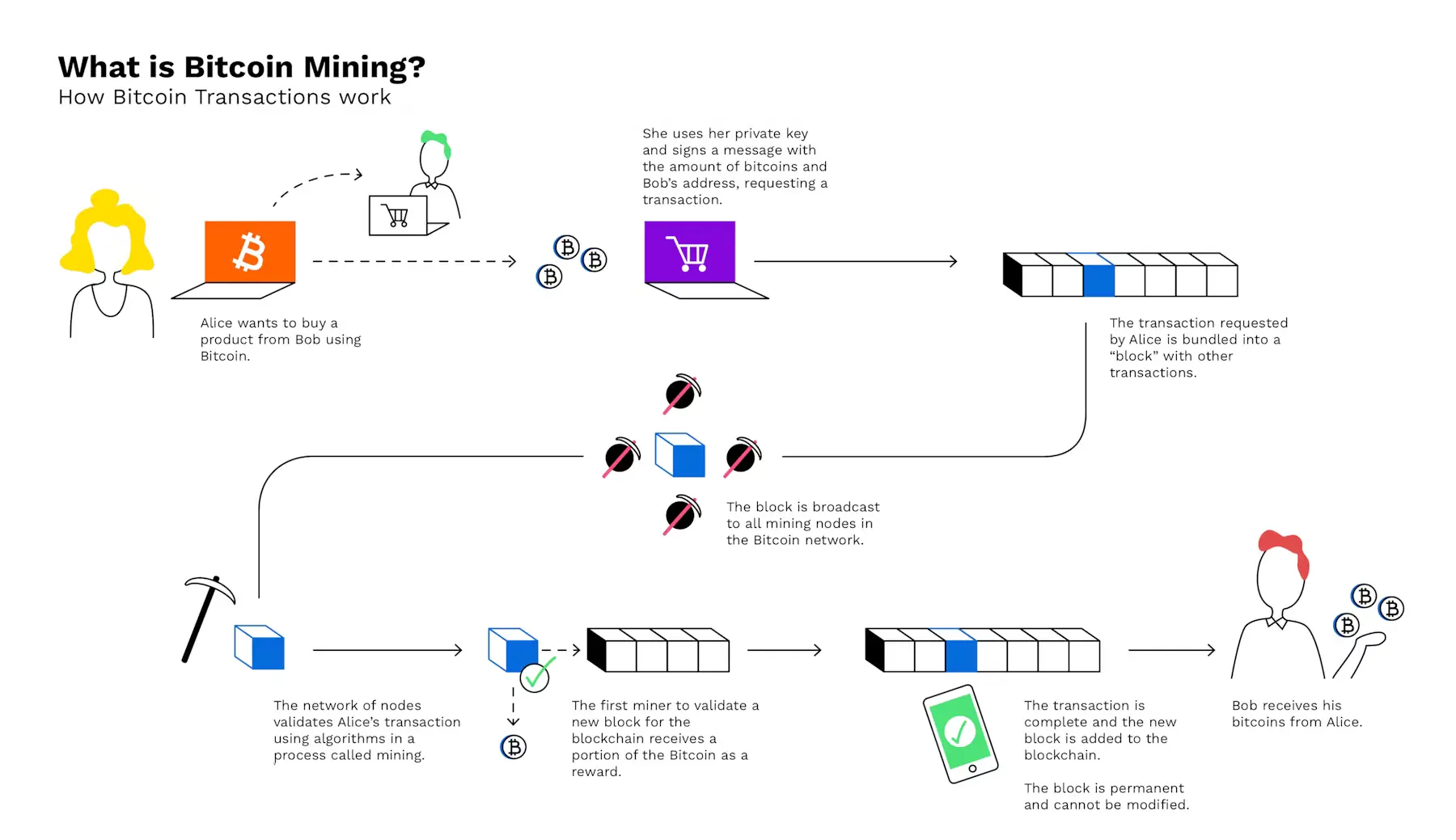

How Blockchain and Bitcoin Are Connected

Bitcoin was conceptualized in 2008 by an individual or entity using the pseudonym Satoshi Nakamoto. Nakamoto published a document explaining a novel way to transfer money directly from sender to recipient, bypassing financial intermediaries. In the same document, the concept of blockchain was introduced as the foundation for Bitcoin. Blockchain incorporates cryptographic principles, hence the term cryptocurrency for this new form of currency exchange.

Bitcoin is considered an asset similar to gold, silver, or other metals, leading to its mining process being referred to as "mining." The computer that first calculates the correct pair of nonce-hash or lock-key receives a commission for all transactions mined in a specific block. This helps the computer owner or a farm of computers to offset equipment expenses and earn income.

It turns out that Bitcoin or any other cryptocurrency is not just an asset but also the fuel for the blockchain. This allows maintaining the stability of the crypto model even after the issuance of new coins ceases.

Advantages and Disadvantages of Blockchain Technology

Advantages:

- Decentralization: Blockchain operates on a network with no single central authority, providing greater security and resistance to attacks.

- Data Security: Blockchain uses cryptographic methods to protect data. Each transaction or record in the blockchain is stored as a hash, making it reliable and secure against unauthorized changes, fraud, and malicious access.

- Transparency: Beneficial in sectors where tracking and confirming the transaction history is crucial. For example, in the supply chain and logistics industry, blockchain can help trace the path of a product from the manufacturer to the consumer.

Disadvantages:

- Energy Consumption: Mining and transaction processing in blockchain require a significant amount of computational power and energy. For instance, Bitcoin mining consumes a vast amount of electricity—this can negatively impact the environment.

- Immutability of Data: Once data is recorded on the network, it is challenging to alter and practically impossible to delete. For example, if incorrect information about property rights is stored in the blockchain, rectifying it would be difficult without the intervention of a majority of network participants.

- Risk of Majority Attack (51% Attack): If a group of attackers manages to control 51% of a blockchain, they gain control over it. Manipulations with assets in such a network can occur disguised as regular transactions. While the likelihood of this happening is low—requiring substantial resources and coordinated effort—it remains a systemic drawback that cannot be entirely eliminated.

Applications of Blockchain Technology

Using Bitcoin as an example, we have already established that blockchain enables secure transactions without intermediaries. One blockchain that is currently utilized for international money transfers is RippleNet. Banks and other financial institutions can conduct international transfers on this platform using digital assets like XRP, reducing the time and cost of transactions. However, blockchain technology can be applied not only to transactions but also in various other ways. Here are five additional applications:

- Decentralized Applications (DApps): Smart contracts pave the way for the development of decentralized applications (DApps) that operate on the blockchain, offering new ways to organize economic and social interactions. For instance, in the social network Yup, users can create collections of content from the internet through a browser extension and appreciate collections from others.

- Supply Chain and Logistics: Blockchain allows for tracking and recording every stage of the supply chain process, from the manufacturer to the consumer. For example, Walmart uses blockchain to trace and confirm the path of products from the farm to the store. This helps quickly identify and address issues in the supply chain.

- Healthcare: Blockchain can store electronic medical records, medical histories, and laboratory test results. For instance, the MedRec project uses blockchain to store patients' medical data, ensuring their confidentiality.

- Voting and Elections: A blockchain can establish an electronic voting system where each vote is securely recorded, and the election results are impossible to alter or counterfeit.

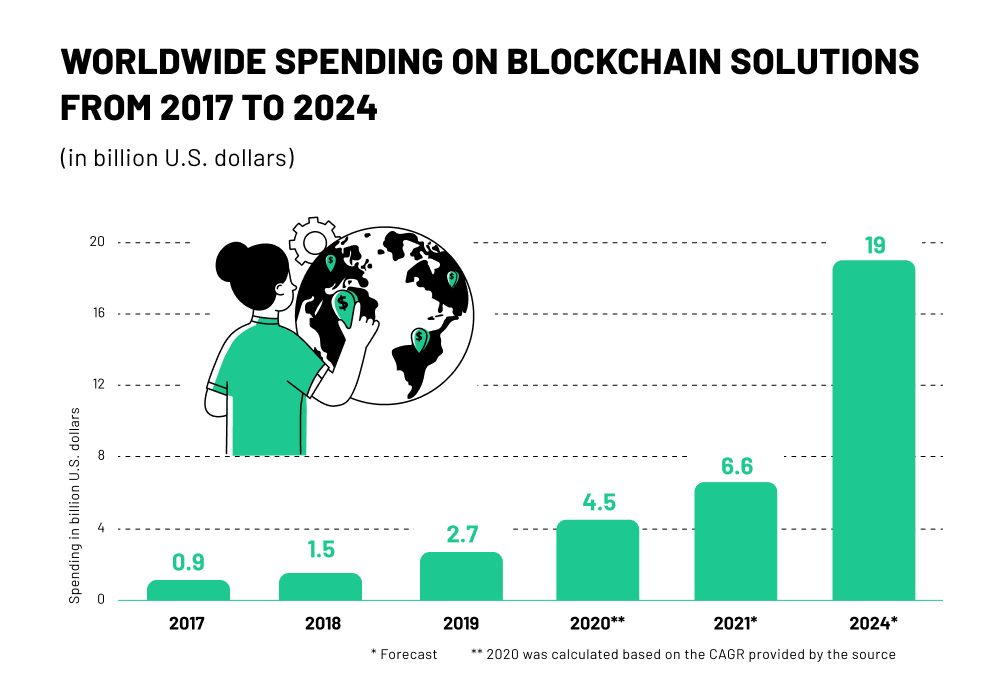

The Future of the Technology

Statistics on the use of blockchain in various industries indicate that it will be increasingly adopted in the future. For example, according to a PwC study, as early as 2018, 84% of companies were either exploring or actively engaged with blockchain. Major entities such as IBM, Walmart, Maersk, and JPMorgan Chase have already implemented blockchain solutions into their processes. Analysts anticipate that blockchain spending will nearly triple by 2024 compared to the figures from 2021.

The flip side of blockchain is its drawbacks. Due to these, the technology may spread more slowly. Here are the issues that need to be addressed to increase the number of blockchain projects:

- Scalability: To address this issue, new consensus algorithms and solutions need to be developed to speed up processes in the network and reduce the cost of using blockchain technology.

- Regulatory Environment: Data protection, privacy, and identification issues need to be defined and standardized to instill more trust in blockchain solutions.

- Blockchain Integration: Developing standards and protocols to enable different blockchains to exchange data and interact with each other.

- Gray Image: Blockchain and cryptocurrencies are often associated with high-risk investments and underground transactions. It's important to educate people and companies about the benefits and possibilities of the technology.

- Environmental Issues: Cryptocurrencies that operate on the Proof of Work principle consume a significant amount of electricity for mining. To mitigate the harm from such blockchains, alternative consensus mechanisms like Proof of Stake will need to be considered.